Despite the non stop rally in the price of gold for over a decade, every normal pullback has been proclaimed as “the end of the gold bull market” by the mainstream media. Will gold eventually become an over-owned and overpriced asset? Yes – but that day will not arrive until gold is many thousands of dollars higher. Long term gold investors who have stayed with the primary trend have already outperformed every other asset class over the past decade as shown in this neat infographic from the Visual Capitalist.

visualcapitalist.com

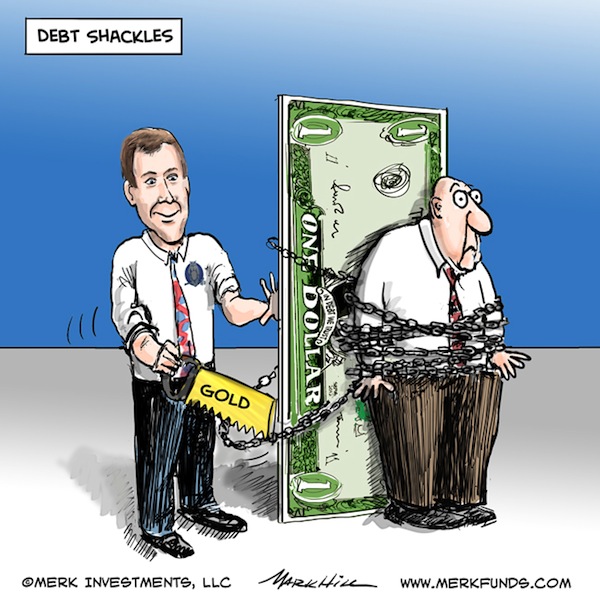

By Axel Merk

By Axel Merk

By Axel Merk

By Axel Merk By

By

Legendary bond king investor Bill Gross, who presides over the world’s largest bond funds makes a compelling case for owning gold in an interview with Bloomberg TV. Lead manager of influential Pacific Investment Management Company (PIMCO) since 1987, Bill Gross reputedly made $200 million in 2011.

Legendary bond king investor Bill Gross, who presides over the world’s largest bond funds makes a compelling case for owning gold in an interview with Bloomberg TV. Lead manager of influential Pacific Investment Management Company (PIMCO) since 1987, Bill Gross reputedly made $200 million in 2011. India may increase the import tax on gold for the third time this year in an attempt to shore up the weak rupee. Purchases of gold and silver account for a huge 12.5% of all Indian imports and are contributing to a record current-account deficit according to

India may increase the import tax on gold for the third time this year in an attempt to shore up the weak rupee. Purchases of gold and silver account for a huge 12.5% of all Indian imports and are contributing to a record current-account deficit according to

The latest sales figures from the U.S. Mint for August show a significant increase in sales of both gold and silver bullion coins.

The latest sales figures from the U.S. Mint for August show a significant increase in sales of both gold and silver bullion coins.

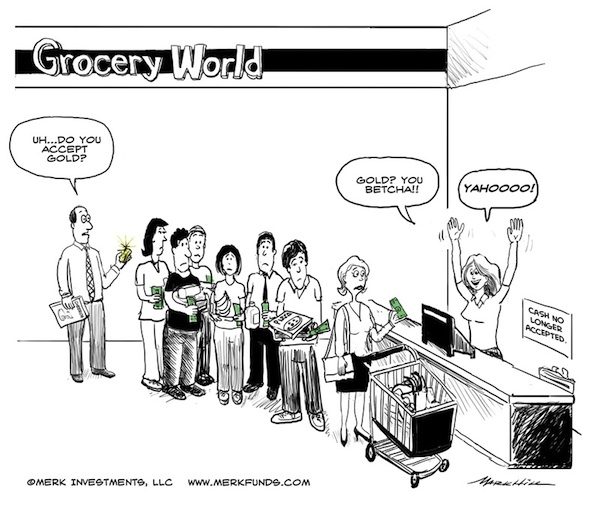

By Axel Merk

By Axel Merk

Yahoo Finance ran a story today entitled “Gold, Silver & Copper Are All Heading Lower.” Nothing worth discussing about the specifics of the article – the real story here is that this a classic contrary headline seen at market bottoms, not tops.

Yahoo Finance ran a story today entitled “Gold, Silver & Copper Are All Heading Lower.” Nothing worth discussing about the specifics of the article – the real story here is that this a classic contrary headline seen at market bottoms, not tops.