MOTIVE: The various governments of the world and their central banks produce and distribute a product – paper currencies. Those currencies are backed by confidence, faith, and credit, but not by gold, oil, or anything real. Those currencies are digitally printed to excess, since almost all governments spend more than their revenues. The UK, Japan, and the USA are prime examples.

MOTIVE: The various governments of the world and their central banks produce and distribute a product – paper currencies. Those currencies are backed by confidence, faith, and credit, but not by gold, oil, or anything real. Those currencies are digitally printed to excess, since almost all governments spend more than their revenues. The UK, Japan, and the USA are prime examples.

Politicians want to spend more money, but they also need to maintain the illusion that the money is still valuable, that it will retain most of its purchasing power over time, and that inflation is under control. The illusion weakens when food, gasoline prices, and other consumer goods are wildly rising in price. At a more abstract level, gold indicates the same lack of confidence in the printed pieces of paper that our central banks distribute.

Hence, central banks and governments have a strong motive to “manage” the inevitable price increases in gold. They have a motive to suppress the price and to allow it to rise gradually over time, while occasionally smashing it down and temporarily destroying confidence in gold as an alternative to unbacked paper currencies. The press helps by regularly claiming gold is in a “bubble.”

Yes, there is a clear and compelling motive.

MEANS: This brings up a heavily debated topic – do governments and central banks have the means to manage the price of gold? Ask yourself these questions:

- Did banks manipulate rates in the LIBOR market?

- Does the Federal Reserve (and other central banks) set (manage – manipulate) interest rates in the credit markets?

- Do banks exercise considerable influence over regulators and Congress?

- Are the various central banks of the world centers of power and wealth?

- Do they use their wealth and power to achieve their policy objectives?

- If the Fed can create and lend/loan/swap/give away over $16 Trillion dollars after the 2008 crisis, is it possible that some of that $16 Trillion was used to influence the gold market?

- Did Greenspan, when he was Chairman of the Federal Reserve, make a statement in 1998 that central banks were ready to lease gold if the price of gold rose? Link is here.

- If central banks lease gold to bullion banks and those banks SELL that gold into the market, would that have any influence on price?

- Are central banks allowed to claim leased gold, which they no longer physically possess, as an asset on their balance sheet? (Lease it into the market but still claim they have it – this works until they run out of gold or the physical gold is audited.)

Yes, central banks and governments have the MEANS to suppress the price of gold.

OPPORTUNITY: As long as:

- Governments spend more than their revenues

- Central banks and governments control their gold in secrecy

- Physical gold is not audited (last real audit of the USA gold was about 60 years ago)

- Gold can be leased out while being listed as owned,

then there is opportunity.

Further, if a few billion dollars can be created and then used by a futures trader, and that trader sells (naked shorts) a large number of gold contracts on the futures exchange, that will drive the gold price down rapidly. Look at the chart of gold prices for April 11 – April 16 and ask yourself if that looks like a managed market.

Yes, central banks and governments have the OPPORTUNITY to suppress the price of gold.

But there is more to the story!

Central banks and governments have, to one degree or another, the motive, means, and opportunity to manage the price of gold. Clearly, their bias is to hold the price of gold low and to restrict its upward movement. Similarly, they want bond and stock markets to move higher, but that is another story.

YOU have motive, means, and opportunity to protect yourself and to profit from this process.

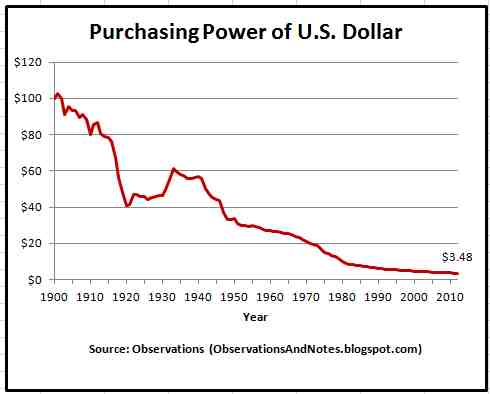

You know that unbacked paper currencies are declining in purchasing power. The path is erratic but clearly lower over the last four decades. You want to protect your purchasing power – you have a MOTIVE to own gold instead of owning devaluing currencies that pay next to nothing in interest.

You probably have paper dollars that are “invested” in stocks, bonds, IRAs, and other savings. You have the MEANS to protect yourself. Sell some paper and buy gold. The Chinese and Russians are doing it as rapidly as they can. What do they see that you might not fully understand?

You have the OPPORTUNITY to buy gold and silver at a huge discount to their real value – just my opinion – but both are “on sale” at current prices. (Gold is currently priced about the same as in late 2010.) “But can’t they go lower?” Yes, of course, gold could drop to $1,000, the Middle East could be transformed into a region of tranquility, peace, and cooperative people, and the US Congress could balance the budget. But as long as governments and central banks are “pushing paper,” digitally printing unbacked currencies, and overspending their revenues, the price of gold will increase – just my opinion – to much higher than it is today.

Gold and silver are in long-term bull markets. One of the objects of a bull market is to arrive at the peak with very few long-term participants. The “bull” wants to buck you off periodically. It usually happens. Basic human nature – fear and greed – makes it difficult to ride the bull most of the way up and exit at the proper time. Fortunately for gold and silver bulls, there are many more years of deficit spending and increasing debt that will push metals prices much higher.

Read from the DI: Why Buy Gold?

GE Christenson

aka Deviant Investor

Anything that sound too good to be true, well, you know how that ends.

Anything that sound too good to be true, well, you know how that ends.

Richard W. Fisher, president and CEO of the Federal Reserve Bank of Dallas gave a very interesting speech today, acknowledging that the Federal Reserve policy’s are experimental. No one, including the Federal Reserve, knows how this unprecedented monetary accommodation will affect the economy and the value of the dollar.

Richard W. Fisher, president and CEO of the Federal Reserve Bank of Dallas gave a very interesting speech today, acknowledging that the Federal Reserve policy’s are experimental. No one, including the Federal Reserve, knows how this unprecedented monetary accommodation will affect the economy and the value of the dollar.

April was a brutal month for precious metal investors. Gold ended the month down almost 8% and silver prices tumbled almost 13%. The sell off continued in May with gold down another $60 per ounce to $1,412 and silver down $1.55 to $22.87 per ounce at mid month.

April was a brutal month for precious metal investors. Gold ended the month down almost 8% and silver prices tumbled almost 13%. The sell off continued in May with gold down another $60 per ounce to $1,412 and silver down $1.55 to $22.87 per ounce at mid month.

Large scale liquidation of gold backed exchange-traded products (ETP) sent gold prices into a tailspin during April. Billionaire investor George Soros, who had sold 55% of his holdings in the SPDR Gold Shares (GLD) during the last quarter of 2012, further reduced his gold positions during the first quarter. Soros is a legendary trader and investor who has made billions moving ahead of the crowd.

Large scale liquidation of gold backed exchange-traded products (ETP) sent gold prices into a tailspin during April. Billionaire investor George Soros, who had sold 55% of his holdings in the SPDR Gold Shares (GLD) during the last quarter of 2012, further reduced his gold positions during the first quarter. Soros is a legendary trader and investor who has made billions moving ahead of the crowd. By: GE Christenson

By: GE Christenson

By GE Christenson

By GE Christenson The exploding demand for physical gold and silver has become a worldwide phenomenon. Shortly after the price plunge of early April buyers rushed in to take advantage of bargain prices. Dealers and mints worldwide have reported off the charts demand for physical gold and silver.

The exploding demand for physical gold and silver has become a worldwide phenomenon. Shortly after the price plunge of early April buyers rushed in to take advantage of bargain prices. Dealers and mints worldwide have reported off the charts demand for physical gold and silver.