The basic law of supply and demand dictates the quantity of goods offered for sale. If prices are low and goods cannot be sold at a reasonable profit, producers will be unmotivated to increase production. If prices increase as demand for a product is soaring and producers can reap high returns, supply will increase as producers increase output to maximize profits.

The basic law of supply and demand dictates the quantity of goods offered for sale. If prices are low and goods cannot be sold at a reasonable profit, producers will be unmotivated to increase production. If prices increase as demand for a product is soaring and producers can reap high returns, supply will increase as producers increase output to maximize profits.

When it comes to gold, however, the textbook equation for supply and demand can be thrown out the window. Gold exists in finite quantities and has become increasing more difficult and expensive to mine. In addition, major new gold deposits discoveries have dropped to zero in the past two years and ore grades have declined significantly to only 3 grams per tonne from 12 grams per tonne in 1950.

Even as gold exploded in price from under $300 per ounce in 2002 to $1,800 per ounce in 2011 gold production trended lower. Despite much higher prices, gold miners were simply unable to increase supply. According to the World Gold Council mine production over the past five years has not increased and average annual production has remained stable at approximately 2,690 tonnes per year.

On a long term basis gold production will continue to decline even further for the simple reason that most of the earth’s richest deposits of gold have already been mined and new gold deposit discoveries have declined significantly (see New Gold Discoveries Decline by 45%).

At the end of 2012 it is estimated that all the gold ever mined in history totaled approximately 173,000 metric tonnes. According to the Perth Mint, a study done by Natural Resource Holdings estimates that there are only about 56,674 metric tonnes of recoverable gold reserves left. If this bleak assessment is correct, over 75% of the world’s total gold reserves have already been mined as shown in the infographic below.

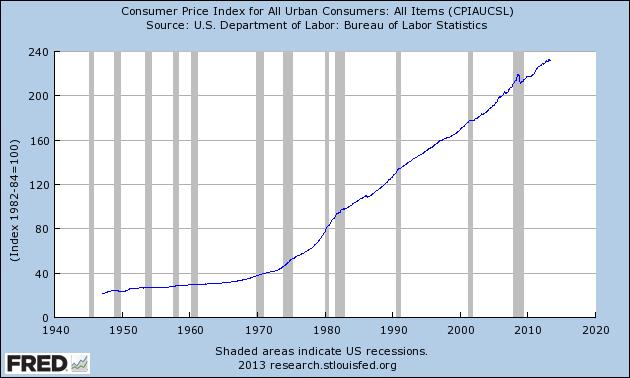

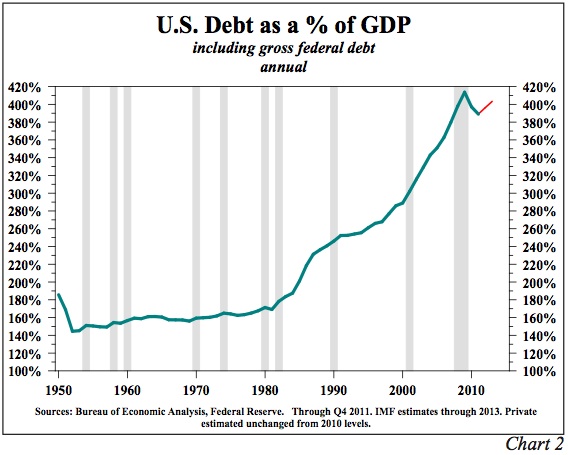

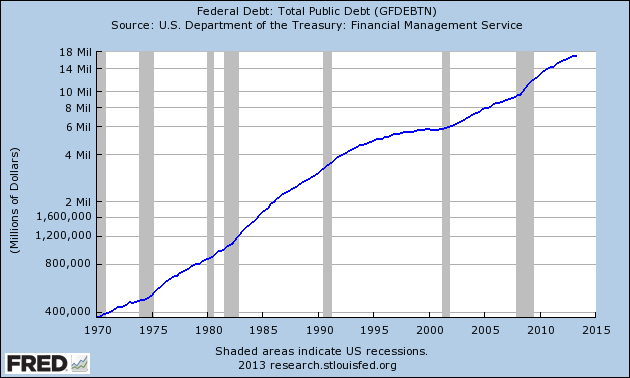

To keep things in perspective, the total global gold supply (including both mined gold and gold reserves) totals 230,000 metric tonnes worth about $9.2 trillion at the current gold price of $1,239. By comparison, the U.S. deficit has exploded to over $17.2 trillion and the Federal Reserve has printed $4 trillion to drive down interest rates by purchasing mortgage backed securities and treasury debt.

In the bizarro world financial system created by the Federal Reserve and other central banks, the meaning of money has become distorted to the point where it is almost meaningless. The recent decline in gold prices should be viewed as a long term opportunity to increase positions in a currency that central banks cannot create at will in infinite quantities.

By: GE Christenson

By: GE Christenson

Let’s back away from the “smaller” questions like:

Let’s back away from the “smaller” questions like:

The American public’s love affair with the U.S. Mint American Eagle silver bullion coin continues unabated. Ever since the financial meltdown of 2008 there has been an explosion in demand for the silver coins. Average yearly sales of the silver bullion coins have increased by almost 500% since 2008 and sales for 2013 are on the verge of shattering all previous yearly sales records.

The American public’s love affair with the U.S. Mint American Eagle silver bullion coin continues unabated. Ever since the financial meltdown of 2008 there has been an explosion in demand for the silver coins. Average yearly sales of the silver bullion coins have increased by almost 500% since 2008 and sales for 2013 are on the verge of shattering all previous yearly sales records.

The American Eagle silver bullion coins cannot be purchased by individuals directly from the U.S Mint. The coins are sold only to the Mint’s network of authorized purchasers who buy the coins in bulk based on the market value of silver and a markup by the U.S. Mint. The authorized purchasers sell the silver coins to coin dealers, other bullion dealers and the public. The Mint’s rationale for using authorized purchasers is that this method makes the coins widely available to the public with reasonable transaction costs.

The American Eagle silver bullion coins cannot be purchased by individuals directly from the U.S Mint. The coins are sold only to the Mint’s network of authorized purchasers who buy the coins in bulk based on the market value of silver and a markup by the U.S. Mint. The authorized purchasers sell the silver coins to coin dealers, other bullion dealers and the public. The Mint’s rationale for using authorized purchasers is that this method makes the coins widely available to the public with reasonable transaction costs. Although sales totals vary from month to month, annual sales of the U.S. Mint American Eagle gold bullion coins are running at triple the levels prior to 2008 when the wheels came off the world financial system and central banks began an orgy of money printing.

Although sales totals vary from month to month, annual sales of the U.S. Mint American Eagle gold bullion coins are running at triple the levels prior to 2008 when the wheels came off the world financial system and central banks began an orgy of money printing.

In an interview with CNBC, former GOP presidential candidate Ron Paul endorsed the efforts of his son, Senator Rand Paul, to hold up the nomination of Janet Yellen as Federal Reserve Chairman until laws are passed requiring more transparency from the Fed.

In an interview with CNBC, former GOP presidential candidate Ron Paul endorsed the efforts of his son, Senator Rand Paul, to hold up the nomination of Janet Yellen as Federal Reserve Chairman until laws are passed requiring more transparency from the Fed.

By: GE Christenson

By: GE Christenson